I’ve noticed a trend in the frugal community to reduce spending in small areas. Small areas of the budget include items like brands of food, cleaning products, small maintenance items, school supplies, clothing, and convenience items (e.g., take-out coffee). I’m all for reducing spending on items that don’t make much of a difference to your livelihood. I’m also in favor of reducing mindless spending, primarily because many of our smaller purchases often fail to match up with our values and goals.

Why Cutting Small Might Not Help As Much As You Think

The flaw with focusing on reducing dollars spent on small items, is that it distracts us from many of the bigger items that will account for much more of our financial success.

Focusing on smaller items, instead of bigger items is common in all aspects of life. I used to work with a boss who redid the office seating chart whenever there was a personnel change. There were a lot of items for my boss to focus on. One of the least important, and easiest to delegate, was figuring out who sat where in a small office. Yet, instead of focusing on bigger company issues, he worked on the new office layout. I often wondered why he had time for seating, but not time for legislative strategy. Later, with experience, I understood that it was easier to address small problems than large problems, even though addressing just one large difficult procurement, would result in better outcomes than the annual office layout review.

We often focus on small items, because small wins give us immediate gratification. Switching brands of frozen peas and bringing our own coffee to work offer an immediate sense of virtue, and is also relatively easy to execute. Yet these areas also account for a relatively small portion of our budget, compared to housing, transportation, and debt payments (credit card, loans). Making one change in one large category is nearly always more effective than making changes in several small categories.

Let’s say you want to pay off some debt early, because the interest is high, and you want to start saving for a car. You have $16,000 in student loans, and you’d like to pay them off in the next three years. You don’t intend to take on a second job, so you need to find some place to reduce costs. You could brown bag it, and go out to the movies less. Or you could reduce your single largest expense, which for most of us is housing. The two main ways to reduce your housing expense is to find cheaper lodging, or to bring in a roommate to your current location.

Technically, from a budgeting standpoint, bringing on a roommate increases your income, and does not decrease your rent/mortgage, but I combine the concepts here, to make a point about focusing on your largest expense areas.

Going Big Is Better

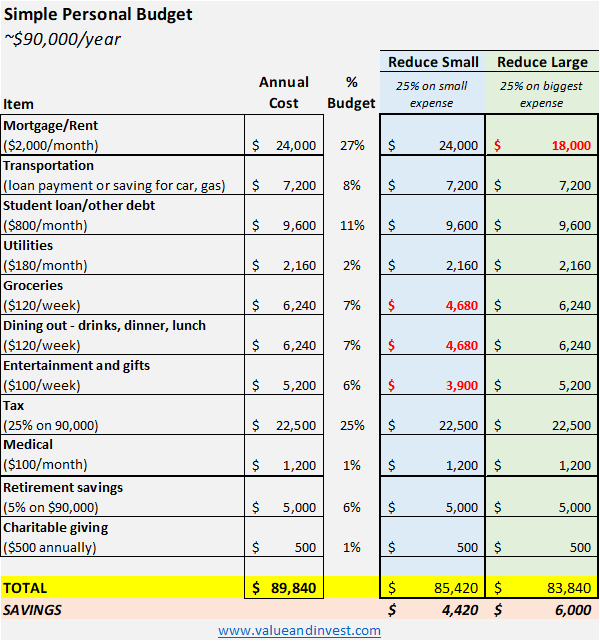

For those that like numbers, this table compares how reducing small areas by 25% compares to reducing your largest area by 25%.

In this budget, housing accounts for over 27% of annual expenses. Excluding taxes, nothing else comes even remotely close. The numbers in red indicate a 25% reduction. If you reduce several small areas by 25%, you save $4,420, but if you reduce your single largest expense area by 25%, you save $6,000 each year. If you can reduce your housing expense by $500/month through a cheaper location or a roommate, you could make no other changes, and still wipe out your student loans in less than three years.

The 25% Rule

The best way to figure out which areas will result in the biggest savings outcomes is to focus on anything that is 25% or more of your annual spending. Then, reduce your highest area of spending by 25% or more.

Where do you apply the savings? First to debt, later to an emergency fund. In this scenario, the student loan debt is retired in less than three years, and a 3-month emergency savings fund is established in less than two years. This assumes no other adjustments to living, and no pay increases. You still contribute to retirement. You still buy coffee and lunch. You still go to the movies. Arguably, it may be easier in the near-term to forgo small expenses, rather than figuring out the larger areas. But the gains are nearly always less.

If you don’t have a single area of that accounts for 25% of your spending, go down to 20%. My husband and I made this work for us, by keeping our housing costs to 15% of our income. We were free to use the savings toward paying down debt, investing, retirement savings, a new-to-us car, or something fun.

Using the 25% rule can help you determine that areas that will be most effective in reaching your goals, and allows you to make a single decision, rather than making many small decisions each month. Focusing on the biggest areas is, in fact, just as rewarding as the small.

Photo by Alexei Scutari on Unsplash